Shut up of a senior couple obtaining breakfast and performing costs

istock

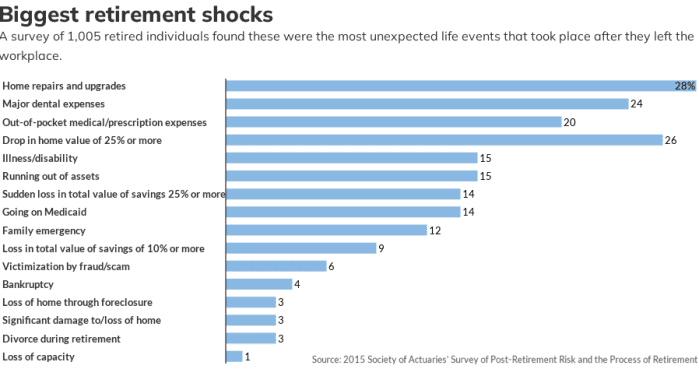

Only about 1 in 4 retirees has not knowledgeable any sort of shock occasion in retirement, in accordance to a review from the Society of Actuaries. And these shock activities — like a massive dental monthly bill, for case in point — often arrive with a shock price tag as well. That can be specifically tricky for retirees, as contrary to when someone is doing work and making a continual paycheck, retirees’ should rely on their long-term setting up and set month to month distribution checks.

The very good news? Bolstering your discounts can safeguard towards these shock functions. “With retired purchasers, one particular of the bigger merchandise that we communicate about is how a lot of months of distributions we want to established aside for additional income for unforeseen, or irregular bills,” reported Peter T. Palion, certified economic planner and president of Master Plan Advisory in East Norwich, New York. (See the very best price savings account charges you may perhaps get below.)

Caring for cherished ones

This is one particular of the most unexpected expenditures in retirement, and features the clinical requirements of a wife or husband, dad or mum, baby or grandchild, claims Spencer Betts, a licensed economic planner, main compliance officer and financial advisor at Bickling Economic in Lexington, Massachusetts.

“These are virtually difficult to predict, but using care of someone’s long-time period treatment demands can get particularly highly-priced,” he states, incorporating that this form of care could also contain helping a beloved 1 with addiction, a divorce settlement, bankruptcies and other money centered requires. “Not only will this choose economic sources but could include things like relocating and hours and hrs of individual time.”

Caregiving brings about a fiscal strike: For example, spousal caregivers in between the ages of 59 and 66 had 50% less in IRA property, 39% much less in non-IRA belongings and 11% a lot less in Social Safety profits, as perfectly as much less earnings than married non-caregivers, the report discovered.

But organizing for this period can be in particular difficult due to the fact of the big cost differential dependent on the treatment wanted, suggests Betts. “On the reasonably priced aspect there is simple treatment, like a touring nurse that arrives to your household a few periods a 7 days and tends to make certain you are having medicines and aids with some basic tasks. On the extra highly-priced aspect are Alzheimer models that offer spherical the clock monitoring of aged people.”

The very first phase when it comes to setting up for this stage of life is “to search at your family’s health and fitness record,” Betts stated. In addition to thinking of very long-expression care insurance policies, he says that it is also very important to look into “the price tag of care around wherever you stay or exactly where you would like to retire,” as that can “vary considerably centered on your location.”

See the ideal personal savings account costs you might get listed here.

Health fees

Partners who are 65 or more mature can expect to spend around $315,000 immediately after-tax bucks on health and clinical fees during retirement, a study from Fidelity uncovered.

That stated, it should not be a surprise that virtually just one-fifth of retirees say they are surprised by sizeable out-of-pocket medical and prescription fees, in accordance to the Culture of Actuaries report. “This does not include if a client wishes to go to some form of assisted residing problem exactly where they can have a person cook dinner for them or have a nurse that checks in on them,” according to Christopher Lyman, a economical advisor at Allied Economical Advisors in Newtown, Pennsylvania.

A report from RBC Prosperity Administration observed that nutritious 65-year-olds can assume to a single day expend as considerably as $100,000-for every-yr on extended-time period charges, which consist of nursing properties, residence care or hybrid solutions.

Lyman states a important component of setting up for retirement is factoring in your wellness and your anticipated high quality of lifestyle. You will need to have to account for additional money for professional medical specialists and drugs in your senior yrs, he said.

Residence repairs

All-around 76% of individuals ages 65 to 79, and 68% of those about the age of 80 are presently residing in single-family members households, according to a exploration report from the Joint Center For Housing Research at Harvard University. In addition, just about three-quarters of folks 50 and older say they would favor to keep in their recent homes as they age, in accordance to an AARP examine.

With this a lot of seniors owning and living in their personal houses, the Culture of Actuaries report discovered that 28% will one particular day experience sudden repairs or undertake big dwelling updates in retirement. The report also identified that 16% of retirees said they ended up shocked by their house price dropping by more than 25%.

When it will come to preparing on household repairs in retirement, nonetheless, Palion always reminds his clients that individuals costs are bound to just one day occur. “If you do all of the property things when you’re not in retirement, you know items break down from time to time and need to have to be set, such as your washing device or sizzling water boiler, or roof or whatever it may possibly be.”

HELOCs or dwelling fairness financial loans and reverse home loans are just some of the likely solutions you may have to beat these unexpected costs.

Betts suggests that when organizing for his clients’ retirements, it’s significant to have more than just one source of income to help buffer any unforeseen expenses relevant to home repairs. “If an surprising cost arises, we have those two additional resources of income that with any luck , will not derail their retirement plans.”

See the finest cost savings account fees you may perhaps get below.

Dental perform

As considerably as surprising expenditures go, main dental function ranks in close proximity to the top rated with 24% of retirees stating they were being stunned with the amount they had to shell out in retirement, according to the Modern society of Actuaries report.

Most seniors can anticipate to shell out much more than $20,000 in dental premiums and extra than $12,000 on shared expenditures from age 65 in 2022 to age 87, according to HealthView Insights analysis. And while Medicare addresses some factors, HealthView Expert services President Ron Mastrogiovanni stresses that it “does not address dental for factors like fillings or pulling a tooth, and which is why people today should strongly look at dental coverage”

To stay clear of unwanted tension and better prepare for these costs in retirement, Palion says to go away the guessing aside and assume you will need to have to expend funds on your teeth in retirement.

“The cost of dental do the job impacts everyone,” he stated. “Everybody has teeth so is it definitely unexpected when you have to have some dental get the job done? Unless of course you have some implants you would want some dental operate.”

Aiding grownup children

As several as 52% of younger grown ups these times, from ages 18 to 29, are dwelling with their dad and mom, in accordance to a report from Securian. That is almost 2 times as numerous did so at the exact age in 1960.

Why is that so really hard to element this in for retirement planning? “We are not able to fiscally product all those expenditures and they usually come about in the course of inopportune occasions these as through a economic downturn,” explained Tom Balcom, CFP and founder of 1650 Wealth Administration in Fort Lauderdale, Florida.

Is there just about anything that can be accomplished to aspect this probable spending into your long-time period financial savings system? Balcom says his company indicates working with adult children on developing their individual spending plan and making sure that they are not overspending their suggests. “I frequently simply call this monetary tough appreciate,” he explained. “If you’re producing $50,000-per-yr, you can’t invest $2,000-a-month on hire.”

Balcom’s organization also advises its consumers to store up to six months of monetary reserves in addition to any retirement resources. “With a quantity of hedged investments, our clients are often probably to have something that has appreciated, so the purchase minimal, promote substantial strategy should normally function.”

The tips, suggestions or rankings expressed in this article are those of MarketWatch Picks, and have not been reviewed or endorsed by our industrial companions.