[ad_1]

With summer time winding down, the U.S. inventory market place is set up for a possibly shaky tumble.

“Recession fears are the most possible cause of a retest of the June lows,” claimed Ed Clissold, main U.S. strategist at Ned Davis Investigation, in an Aug. 31 observe. “From a seasonality point of view, a retest could occur in the upcoming many weeks.”

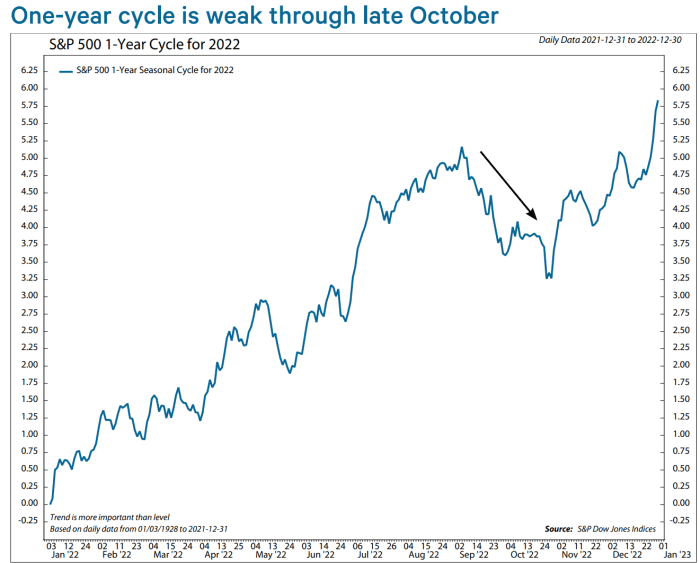

When U.S. buyers return from the lengthy Labor-Working day weekend, heritage signifies they’ll be facing the weakest time of the calendar year for the S&P 500 index: the stretch from Sept. 6 to Oct. 25, according to the observe.

NED DAVIS Investigation REPORT DATED AUG. 31, 2022

The stock industry is currently wobbly.

U.S. stocks closed sharply reduced Friday, with all three important benchmarks struggling a third straight week of losses. Still, the S&P 500

SPX,

ended 7% over its 52-week small of 3666.77 on June 16, according to Dow Jones Industry Knowledge.

“I believe we have to go again and check that level,” stated Bob Doll, main expense officer of Crossmark World Investments, in a cellular phone job interview. “I do not assume the bear industry is automatically more than,” he reported, nevertheless “what I don’t see is a substantial drop from listed here.”

Read: ‘Prepare for an epic finale’: Jeremy Grantham warns ‘tragedy’ looms as ‘superbubble’ may burst

Meanwhile, ongoing desire amount hikes by the Federal Reserve to battle soaring inflation in a slowing U.S. financial system improve odds of a recession together with the prospective clients of this year’s inventory-sector lows becoming retested, in accordance to the Ned Davis notice. The Fed this year is “committed to taking away liquidity from the fiscal system,” building a retest a lot more probably, wrote Clissold.

Vanguard Team reported in a Sept. 1 report that it downgraded its forecast for U.S. financial growth this 12 months immediately after two straight quarters of contraction. The agency now expects economic growth of .25%–0.75% for full-calendar year 2022, down from its estimate very last month of about 1.5%.

“We feel it probably that the United States will struggle to get back previously mentioned-craze expansion in the quarters in advance,” Vanguard reported. “We area the likelihood of a U.S. recession at about 25% in the future 12 months and 65% in the future 24 months.”

Regardless of whether any “retest” of the stock market’s lows is transient may perhaps depend on the capability of the U.S. to keep away from a recession, in accordance to Ned Davis.

“The ordinary non-economic downturn bear lasts about seven months and has declined 25% (-18% above the previous 50 % century), putting the January – June drop in line with the typical circumstance,” Clissold wrote in the Ned Davis notice. “Conversely, the regular recession bear has lasted about a 12 months (17 months about the previous 50 yrs) and declined a suggest of 35%.”

Inflation ‘dragon’

Investors have been anticipating an additional substantial desire amount hike from the Fed at its Sept. 20-21 meeting, soon after chair Jerome Powell sent a crystal clear message in his Jackson Gap speech on Aug. 26 that the central lender would keep battling significant inflation till the task was completed – even if that implies some ache for homes and companies.

Stocks swooned on his remarks that working day, with the Dow Jones Industrial Regular

DJIA,

closing down 1,000 factors and losses have deepened because then.

The “vigorous” rally in stocks seen earlier in excess of the summer season had reflected “too significantly optimism specified we’re however in the early phases of fighting inflation,” reported Crossmark’s Doll. Whilst he thinks inflation has peaked, Doll predicts that its continued drop this yr will very likely be irregular and finish 2022 over the Fed’s 2% focus on.

“It’s not going to stop up at a stage exactly where we say, ‘ok we got that dragon, what is next’?” he mentioned. If inflation, which ran as scorching as 9.1% in June centered on the consumer-rate index, arrives down to 4% or 5%, “that’s excellent information, but it’s not more than enough fantastic news to say the Fed’s completed,” said Doll.

Vanguard expects the Fed to enhance its federal cash fee concentrate on to a assortment of 3.25%–3.75% by yr-close, from around zero at the commence of 2022, in accordance to its notice. That compares with a present-day selection of 2.25% to 2.5%.

Forward of Powell’s Jackson Hole speech, the marketplace narrative had switched absent from the Fed battling inflation by intense amount hikes to, “when are they heading to pivot?” explained Steve Sosnick, chief strategist at Interactive Brokers. But utilizing a comparatively shorter speech, which had “no ambiguity,” Powell turned the target back to financial tightening and the Fed’s unfinished struggle with inflation, sending “a really potent message to the market,” reported Sosnick.

“We’ve been dealing with that ever because,” he explained, pointing to stock industry losses.

“The reality that we’ve moved so far so speedy, and the psychology has modified so speedily, would make me assume that we are nowhere close to looking at the previous of volatility, particularly into the fall,” mentioned Sosnick. “The September-October interval certainly will get additional than its share of marketplace weirdness.”

Inventory-market base?

Equity and quant strategists at Financial institution of The us reported in a BofA World wide Investigate notice dated Sept. 2 that valuations for the S&P 500 keep on being “rich.” In their look at, “a base is not in.”

“Initially, the rally off the June lows appeared far more like a young cyclical bull than a bear current market rally,” said Clissold, in the Ned Davis observe. “Several breadth thrusts and expanding new highs proposed considerably of the drop had run its training course.”

But intermediate-phrase and lengthy-term breadth required to adhere to to ensure a bull industry, he explained, and without the need of that affirmation, “a retest can not be dominated out.”

“The S&P 500 stalled just beneath its falling 200-day moving ordinary and has supplied up about fifty percent of its June 16 – August 16 gains,” Clissold wrote. Also, “the proportion of stocks above their 50-working day relocating averages just skipped its 90% threshold.”

U.S. shares ended Friday with weekly losses, with the S&P 500

SPX,

shedding 3.3% even though the Dow Jones Industrial Normal

DJIA,

fell 3% and the technological know-how-hefty Nasdaq Composite

COMP,

dropped 4.2%.

The U.S. inventory market will consider a crack on Monday to celebrate Labor Working day, resuming trading on Tuesday. The economic calendar for the forthcoming 7 days consists of info on U.S. companies, jobless statements and purchaser credit rating, as very well as the release of the Fed’s “beige guide,” which involves a assortment of organization anecdotes from around the state.

The Fed’s continuation of aggressive level hikes blended with weak point forward for business earnings and the labor industry “is not a strong backdrop for the equity sector,” said Liz Ann Sonders, chief financial investment strategist at Charles Schwab, by cellphone. Also, “we know September, seasonally, tends to be a weak month” for stocks.

[ad_2]